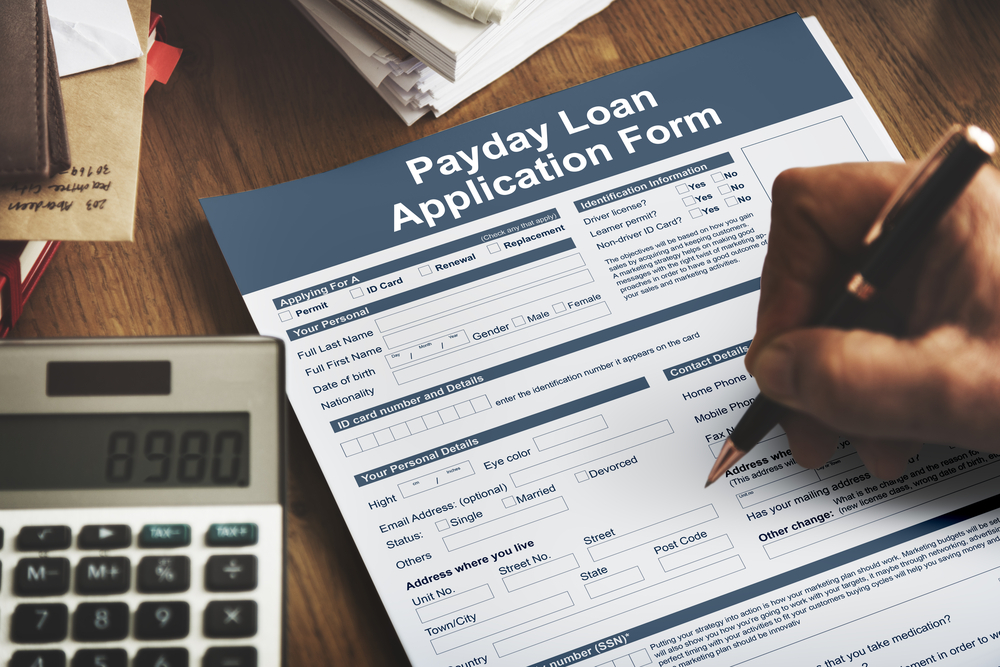

Loan applications are a common thing and they usually come in different types. Today, there is a type of loan known as a Payday loan. They are usually issued upon application and approval to settle short-term financial needs. California Payday loans are the kind of money people borrow to sustain them before payday. They are easy to get since no background check on credit is done for the applicant. They are basically issued in the understanding that the borrower will pay back on the next payday.

When unexpected needs arise before payday, then a payday loan is among the best solution for many people. Instances where payday will be late to address the current needs, a payday loan can come to the rescue. There are very useful on such occasion’s more than conventional bank loans due to low-interest rates and ease of access. Getting online loans in CA is a great solution for those in need of a short-term money solution.

Getting Started with California Payday Loans

The process of getting a payday loan is not complicated. There are no major requirements to meet or scrutiny to be conducted. The process is simple and quick to help borrowers access the money they need at that moment. Application and approval can be done as soon as within a day. Notifications upon approval are sent to confirm availability of funds in the borrower’s bank account.

The money issued as loan is usually due for payment on the next payday! The process gets completed once payment has been done after the borrower receives money on payday. The Payday loan is normally processed electronically. Both applications and processing are conducted through electronic means and that means minimal logistics are required.

Key Requirements for Payday Loans

Payday loans don’t require a credit check for them to be issued out to the borrower. Therefore, those with bad credit can still get payday loans. California payday loans require the borrower to be 18 years of age and of a steady income source. It goes without saying that the applicant should have a valid bank account set up for a direct deposit. These are the basic requirements for anyone who wants to get Payday loans.

All information provided towards the application for a payday loan is kept discretely for the banks use. Therefore, applicants don’t have to worry about their information being shared out. Despite the simplicity in the process, personal details are fully protected for security reasons. As long as the applicant has met the minimum requirements, they are guaranteed the loan despite their credit score. Entrepreneurs in California are constantly creating new businesses and business ideas. However, many may not be aware of the potential benefits to their business which an S corporation provides. For more information consider this resource on forming an s corp in california.

Payday Loan Processing and Approval

To help in the processing and approval of a payday loan, employment and salary information of the applicant is always needed. These details are used to establish the amount of money that can be issued to the borrower as loan. A pre-qualification notice is normally sent to advise the borrower on the amount that can be given as a loan and the details pertaining to it.

Upon receipt of the loan agreement, the applicant is expected to have a keen look at it and make sure that the listed information is credible. Important things to look at include the amount of loan that one qualifies for and the terms of repayment. This comes inclusive of the fees payable for the amount of loan issued to the borrower. All these details are usually stated in the loan agreement form.

As a confirmation that the applicant agrees with the loan terms, they will be required to append their electronic signature on the document. All this is done online and saves the applicant the hassle of printing hard copies for the loan application. Applicants are not coerced to get the loan hence can exit the process at any state. The process is usually completed with funds available in the borrower’s bank account within 24 hours!

Payday loans are short-term loan facilities that help borrows address emergencies. Once an application has been made for a Payday loan, it gets processed and approved based on the minimum loan requirements. This is usually done after a borrower provides the requisite information alongside the application. After that, the money is disbursed into the borrower’s account for their use.